{kind=link}

Estate planning is a crucial step to ensure that your assets are protected and distributed according to your wishes. Taxes can significantly impact the value of your estate if you’re not adequately prepared. It’s essential to understand the tools available to reduce tax liabilities and protect your assets from creditors. By taking proactive measures, you can ensure that your loved ones receive the inheritance you intend for them.

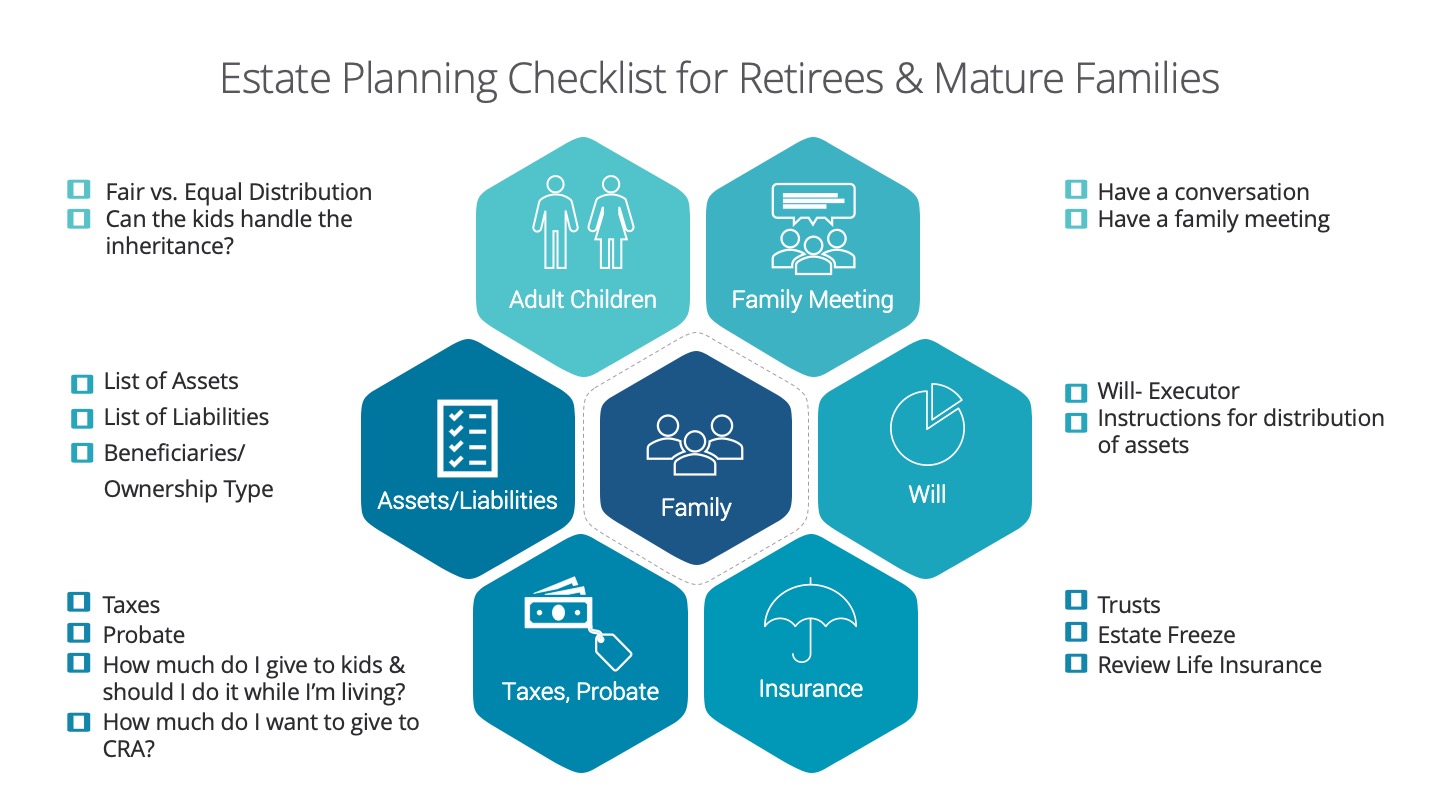

Creating a Will: A Solid Foundation

The first step in estate planning is creating a will. This document provides guidelines on how you want your assets to be divided among your beneficiaries. It’s important to note that a will does not enable your assets to avoid probate. The court will need to verify its validity, incurring costs in the process.

Reduce Your Estate Through Gifting: An Effective Strategy

Gifting is a useful strategy to ensure that some of your assets go into the right hands. In 2024, you can give gifts of up to $18,000 to as many individuals as you wish. Couples can give up to $36,000 to the same person. These gifts do not affect your lifetime gift exclusion amounts. However, it’s crucial to be mindful of the limits to avoid any adverse tax implications.

Charitable giving is another option to consider. You can donate to approved charities through trusts, a will, or directly. Additionally, you can provide the required minimum distribution directly to a charity. It’s important to be aware of the contribution limits imposed by the Internal Revenue Service and other applicable limits.

Create a Power of Attorney Document: Ensuring Your Assets are in Good Hands

A power of attorney (POA) document appoints an individual (and a secondary) to handle your financial and medical affairs in the event of your incapacitation. It’s advisable to consider separate POAs for financial and medical matters, assigning different individuals to each role. Some states even allow the creation of springing durable POAs, which only take effect after you become incapacitated.

Conduct a Roth Rollover: Saving on Taxes

Rolling over an IRA or a 401(k) into a Roth account can help you save money on taxes in the long run. While you will have to pay taxes on the amount you roll into the new account, it can reduce the size of your retirement accounts and subsequently lower your required minimum distributions (RMDs) and taxes. Unlike traditional retirement accounts, Roth accounts do not have RMDs, allowing your money to continue growing tax-free for as long as you want.

Buy Life Insurance: Ensuring Fair Distribution

Life insurance can be a valuable tool to make up for any discrepancies in the distribution of your estate. It can also provide financial coverage for potential heavy medical costs, such as long-term care. By incorporating a life insurance policy, you can ensure that your heirs receive as much as possible without depleting other funds.

Include Non-Physical Assets: Don’t Overlook Important Assets

When preparing your estate plan, it’s crucial to include non-physical assets such as life insurance, retirement accounts, bank accounts, stocks, cryptocurrencies, patents and copyrights, business documents, and more. Additionally, create a separate document detailing how to access these assets, as wills become public after probate is complete.

Start a Trust: A Comprehensive Approach

Trusts are versatile tools that can be tailored to various purposes. They can provide for a disabled child, future education needs, a spouse, or be used as an inheritance vehicle. Trusts can be revocable or irrevocable, with the former allowing for modifications or cancellations at any time. Establishing a trust is beneficial as it removes assets from your estate, reducing your tax liability. Furthermore, assets held in a trust are distributed to beneficiaries more efficiently than those in a will, avoiding probate delays.

A popular trust for many couples is a spousal lifetime access trust (SLAT). This irrevocable trust names the spouse as one of the beneficiaries, allowing them to withdraw assets when needed. However, it’s crucial to consider potential complications, such as losing access to those assets in the event of divorce or the spouse’s death. Including appropriate clauses in the trust document can address these possibilities.

Consult an Estate Planning Attorney: Expert Guidance

While there are online resources available for estate planning, it’s advisable to consult an estate planning attorney for more comprehensive asset protection strategies. They can provide valuable insights and guidance to safeguard your assets from creditors, taxes, and potential challenges to your estate plan.

In conclusion, estate planning is a crucial step in ensuring that your assets are protected and distributed as per your wishes. By taking advantage of various tools such as wills, gifting, trusts, and life insurance, you can minimize tax liabilities and ensure a smooth transition of your assets to your loved ones. Consulting with an estate planning attorney can provide you with expert guidance tailored to your specific needs and circumstances.