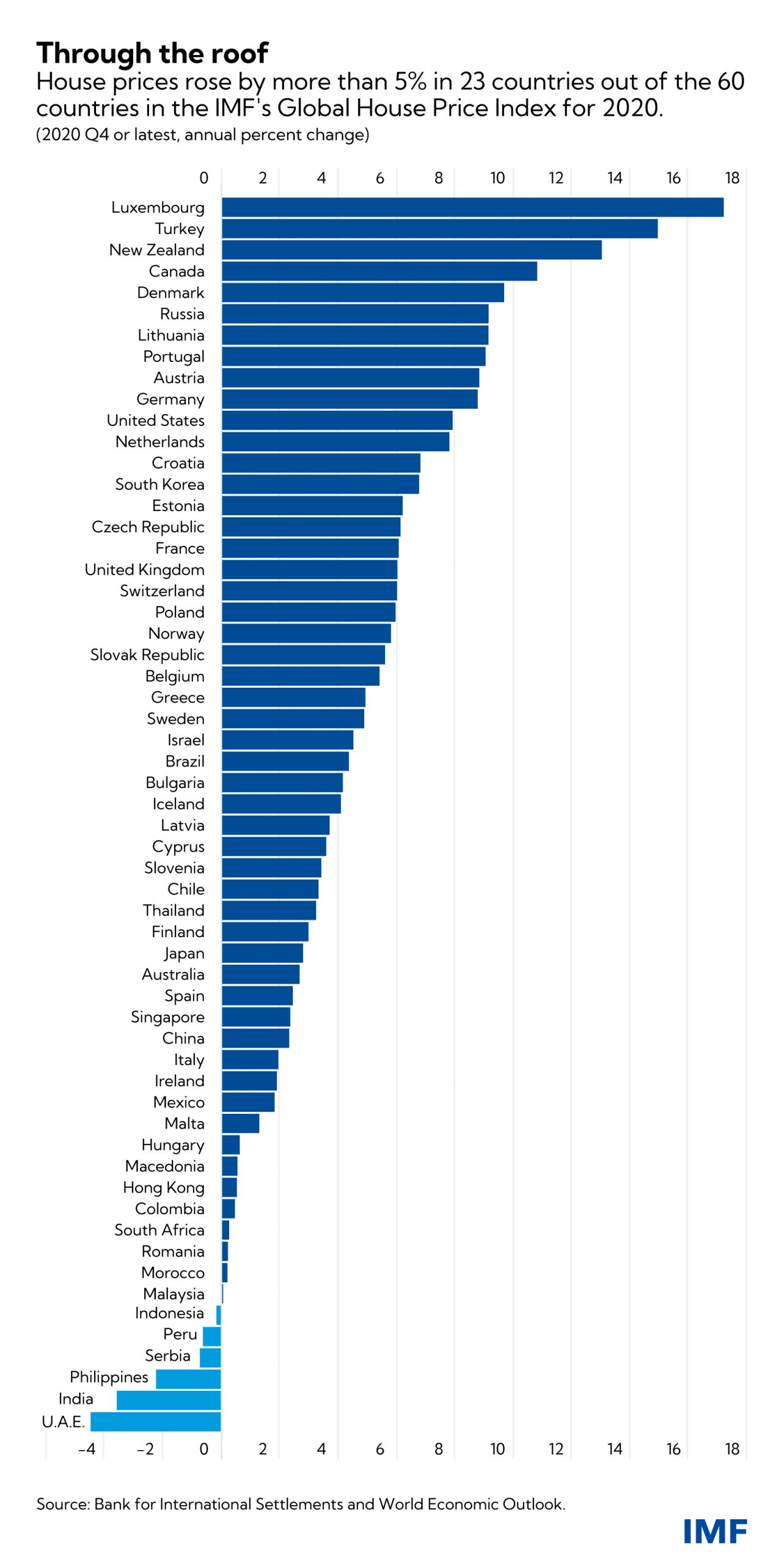

High Down Payments in California Housing Markets

California is home to nine out of the ten cities with the highest down payments in the United States, according to a recent report by real estate data curator ATTOM. The report reveals that prospective buyers in these hot housing markets will need to pay over $180,000 as a down payment to secure a home. The median down payment for homes purchased with mortgages increased by 11.1 percent from the previous quarter, reaching $24,250 in the second quarter.

Leading the pack is San Jose, where the median down payment is a staggering $320,000. San Francisco follows closely behind with a median down payment of $306,375. Other cities in California with higher than $200,000 median down payments include Los Angeles and San Diego. Even cities like Oxnard, Salinas, San Luis Obispo, and Santa Rosa have median down payments exceeding $180,000. Boulder, Colorado also made the list with a median down payment of $195,000.

The rise in down payments is influenced by the current market conditions, where higher-priced turnkey homes in desirable neighborhoods are more likely to sell. Buyers are also opting to put down a higher percentage of the purchase price as a down payment. Redfin, a real estate brokerage, reported that the typical down payment for overall home purchases, including those made with financing and cash, rose by nearly 15 percent from the previous year to $67,500 in June.

The increase in down payments has sparked a political debate, with Democratic presidential candidate and Vice President Kamala Harris proposing to provide first-time homebuyers with $25,000 to assist with down payments. However, this proposal has faced criticism from experts like Kevin O’Leary, the chairman of O’Leary Ventures. O’Leary argues that such policies would fuel inflation and drive home prices even higher.

The high down payments are directly linked to the soaring home prices in these markets. The shortage of properties on the market relative to demand is driving up home prices, making it difficult for aspiring homeowners to save enough for a down payment. In June, the median-priced existing single-family home cost $432,700, a significant increase from $357,100 in 2021, according to the National Association of Realtors (NAR). Redfin predicts that as long as the inventory remains low and the demand for homeownership remains high, home prices and down payments will continue to rise.

Another factor contributing to rising home prices is interest rates. Although rates have come down from the peak of 7.79 percent in late October 2023, they still play a role in driving up prices. Additionally, if mortgage rates were to decrease significantly, it could lead to more bidding wars as more buyers enter the market.

In conclusion, the high down payments in California’s housing markets are a result of the current market conditions, including high home prices, low inventory, and interest rates. While proposals to assist first-time homebuyers with down payments have been made, they have faced criticism for potentially fueling inflation. With home prices expected to continue rising, down payments are likely to remain elevated or increase further.

{kind=link}