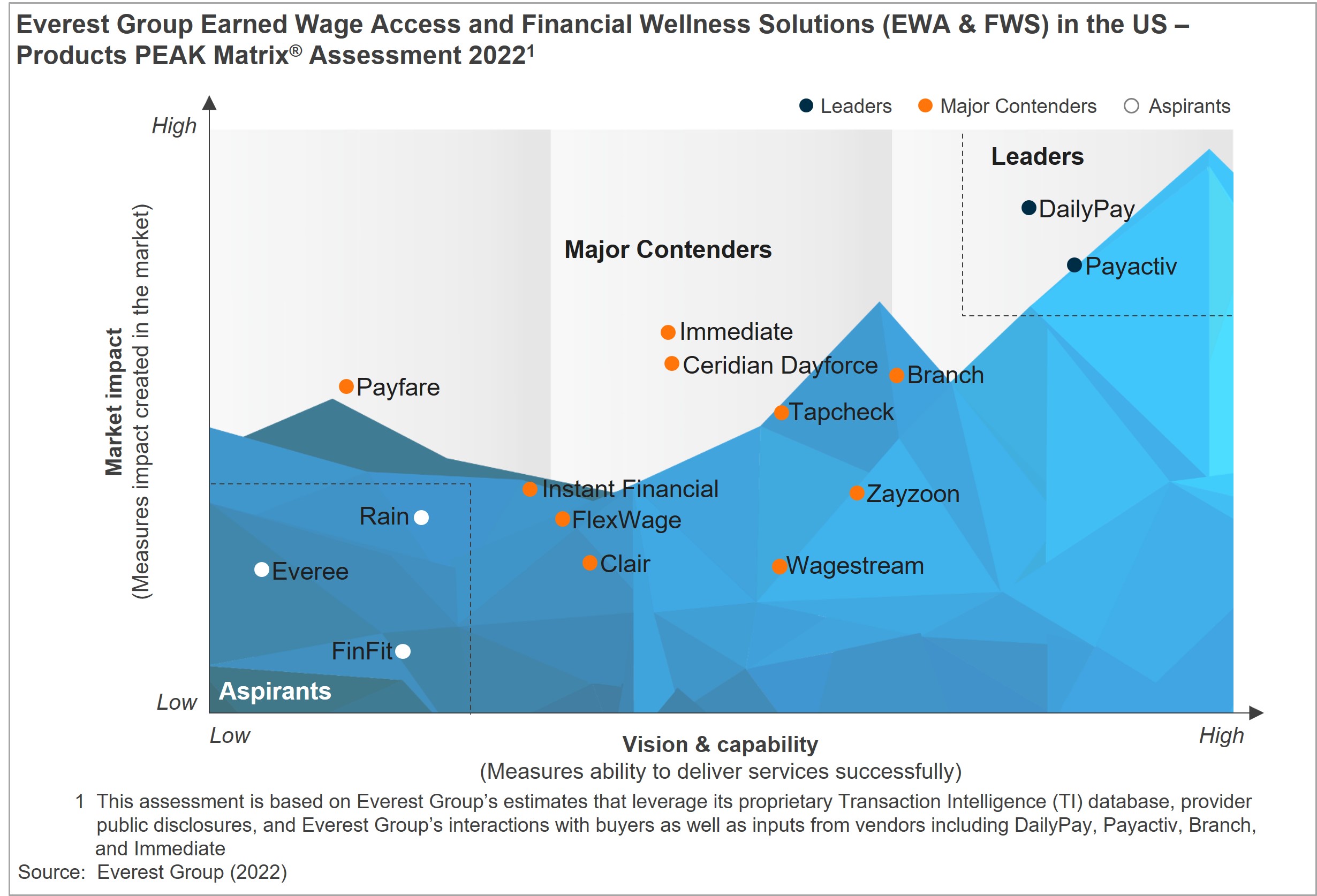

Regulating Earned Wage Products and Buy Now, Pay Later Loans: Impact on Consumer Access to Credit

Regulating Earned Wage Products and Buy Now, Pay Later Loans: Impact on Consumer Access to Credit

Introduction:

The Consumer Financial Protection Bureau (CFPB) recently proposed a rule that would classify earned wage products as consumer loans under the Truth in Lending Act. This move has sparked debate about the potential impact on consumer access to credit.

Earned Wage Products as Consumer Loans:

Earned wage products allow workers to access a portion of their unpaid wages before payday. The CFPB found that interest rates for these products can exceed 100% APR, higher than credit cards. Most of the costs come from expedited fees charged to customers. In response, the CFPB proposed a rule stating that earned wage products are essentially consumer loans and should be subject to accurate cost disclosures.

Criticism from the American Fintech Council:

The American Fintech Council (AFC), representing major financial technology companies, criticized the CFPB’s proposal. AFC President Phil Goldfeder argued that earned wage products are not loans or advances and should not be regulated as such. He claimed that these products provide a safe and reliable alternative to high-cost debt options like payday loans.

Impact on Consumer Access to Credit:

The proposed rule has raised concerns about limiting consumer access to credit. Millions of American families rely on earned wage products, and implementing stricter regulations could hinder their ability to obtain necessary funds. The AFC argues that these products do not require credit checks, underwriting, or impose fees or penalties that affect credit scores.

Need for Regulation:

The need for earned wage products arises from the fact that many workers receive wages biweekly or monthly and may require early access to money for urgent expenses. The CFPB found that workers take out an average of 27 loans per year through these products, with an average transaction amount of $106. The cumulative effect of interest rates, fees, and tips can significantly impact workers’ monthly earnings.

Buy Now, Pay Later Loans:

In addition to earned wage products, the CFPB has also issued a proposed rule targeting “buy now, pay later” loans. These loans allow consumers to make purchases and pay for them in installments without interest. However, the CFPB found that 13% of buy now, pay later transactions involved disputes or returns.

Regulating Buy Now, Pay Later Loans:

The proposed rule requires buy now, pay later lenders to investigate consumer-initiated disputes. During the investigation, lenders must pause payment requirements and issue credits when necessary. This rule aims to address consumer complaints related to disputed transactions and refunds, which amounted to $1.8 billion in 2021.

Conclusion:

The CFPB’s proposed rules on earned wage products and buy now, pay later loans have sparked a debate about consumer access to credit. While the CFPB aims to protect consumers from high costs and predatory lending practices, critics argue that these regulations could limit options for those who rely on these products. Balancing consumer protection with access to credit will be crucial in shaping the final rules.

{kind=link}